This joint article by Mr P. Zacharioudakis and Mr S. Leoussis of Ocean Finance and Dr D. Lyridis of NTUA, is a short introduction to shipping market forecasting. It is imperative to mention that the procedures introduced have a distinct advantage over currently used analysis techniques and apart from their academic value can be used effectively in practical applications. The question is whether the shipping industry is ready to accumulate this kind of innovation. By carefully examining other markets, especially stock markets, we can see that despite the initial reluctance towards change, if there is substantial profit involved, new procedures always find their place.

Article published in financial newspaper “Naftemporiki”.

A popular definition of “forecast” is that it is a reference to future trends usually in the form of probability that is realized by processing and analyzing available data. Then a set of questions slip into mind: In a volatile market such as the one of shipping freight rates, is it possible to acquire information regarding its future evolvement? How can we predict the events that will influence the future state of the market? In this article we will try to answer the above questions and introduce the latest scientific developments regarding forecasting in the shipping market.

The state-of-the-art in the simulation of the shipping market and in the development of methodological tools for forecasting freight rates is the technique developed in the Area of Maritime Transport of the School of Naval Architecture and Marine Engineering in the National Technical University of Athens (NTUA). The research performed in the area has been validated by various practical applications in the forecasting of freight rates for a number of years and for various ship types (tankers, bulk carriers, etc.) Furthermore, its innovation, efficiency, and robustness have been recognized by the international scientific community in many ways and especially by receiving the first prize of the Conference of the International Association of Maritime Economists (IAME 2004) (the specific published paper being: “A multi-regression approach to forecasting freight rates in the dry bulk shipping market using artificial neural networks”), where papers from leading universities from around the world (CASS Business School, MIT, etc.) have been presented.

The tools developed in this work have been applied in modeling shipping markets by Ocean Finance a company dedicated to financial consulting in the field of maritime economics. Ocean Finance is the first company to introduce the FORESIM TM methodology for simulating the shipping market. This is a methodology that combines Artificial Neural Networks, hybrid tools, such as Adaptive Network-based Fuzzy Inference System (ANFIS), data mining techniques, and expert judgment and it provides accurate short- to mid-term forecasts. The results may also be used for risk management.

The procedure for realizing a forecast has been described in various publications of the Area of Maritime Transport of the School of Naval Architecture and Marine Engineering in the National Technical University of Athens. The first step is the definition of the system and the variables to be forecasted. In order to be more specific we will concentrate in the bulk and the tanker markets. Both markets operate in a system with numerous interactions and independent variables that can be divided in two major categories. The first has to do with variables related to demand for transport in and the second with those that are related to the supply of tonnage. The importance of investigating these sets of variables is very high since they determine the freight rates as the result of the equilibrium between supply and demand. Presently, market equilibrium is influenced by the increased demand for sea transport mainly caused by the growing economies in Asia (China and India). Thus, in the near future, and until all new buildings are operational, the market will be demand-driven. A few from the variables used in modeling the market are the following:

- Freight rates

- Active fleet

- Demand for transport in the specific market

- Orderbook

- Demolitions

- Laid-up vessels

The interaction of the market and the variables is either direct or indirect according to the way and the time lag they interact. For example VLCC rates have a direct and positive correlation with the orderbook in realtime. As the observed phenomenon of the Shipping cycle describes, following a high freight rate period new vessels enter the market resulting into an increase in the total transport capacity and subsequently into a drop in the rates. Therefore, the two variables have a negative correlation when examined under a specific time lag. All variables, except for demand for sea transport, are in some way correlated to market trends and vice versa. However, demand for sea transport is determined by other factors and not by the state of the shipping market. For example, while the level of oil production by OPEC has a strong influence in the market, there is no feedback from the shipping market to the level of oil production. But which are the variables that influence demand in the shipping market? In the case of VLCC carriers the demand is related to the following:

- The growth of world economy

- Oil shocks

- War – hostile acts near oil production facilities

- Oil reserves

- Oil price

- Climate conditions

- Political decisions – OPEC policy

- New reserves

Forecasting the need for sea transport is very difficult since it is related to quantitative and qualitative variables with unforeseen trends. What can be done is to “feed” the forecasting model with different scenarios and generate a stochastic ‘description’ of the future. This is why FORESIM TM was conceived as a complet forecasting procedure.

FORESIM TM can generally be described as a simulation procedure applied in the shipping market. The procedure was developed in order to produce future freight rates realizations depended to the current state of the market. The procedure is the first to introduce the concept of generating freight rate realizations conditional upon the current or the preceding market states and of embedding explanatory and stochastic modeling. Therefore, it creates tool for acquiring quality information regarding the trend of the market taking into consideration unforeseen parameters as well as the present status of the market.

The main applications of FORESIM TM are the following:

- Decision support for trading Future Freight Agreements (FFAs) and various shipping market derivatives;

- Chartering strategy – spot or time charter, duration, etc.;

- Risk management for shipping investments, in combination with cash flow and monte carlo simulations providing distribution for financial variables;

- Estimation of financing risk such as probability of default etc.

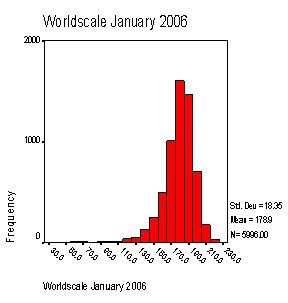

Example of VLCC Worldscale distribution

for January 2006 using data up to July 2005.